Since online transactions are commonplace, businesses must provide dependable and secure payment options to satisfy their clientele. By streamlining their operations, automating payment processing, and leveraging efficient payment solutions to manage financial transactions, businesses can enhance their overall performance in the competitive online market.

This process usually involves the role of certain intermediaries, like payment aggregators and payment gateway service providers. These entities create a link between customers and merchants, facilitating digital (cashless) transactions between them. Besides, many E-Commerce and M-Commerce service providers have also been providing such online platforms for digital payments. However, we will be discussing the payment gateway aggregator in detail.

Who Are Payment Gateway Aggregators?

A payment aggregator serves as an intermediary between consumers and businesses. It is a third-party provisioner that enables consumers to make quick and easy payments, allowing merchants to manage their transactions more efficiently.

A payment aggregator allows businesses to accept transactions in various formats from many bank accounts or financial institutions without having to open a merchant account in each bank (where they may receive payments). They are incorporated into merchants’ websites or apps to accept payments via card transactions, e-wallets, and account transfers, among other options.

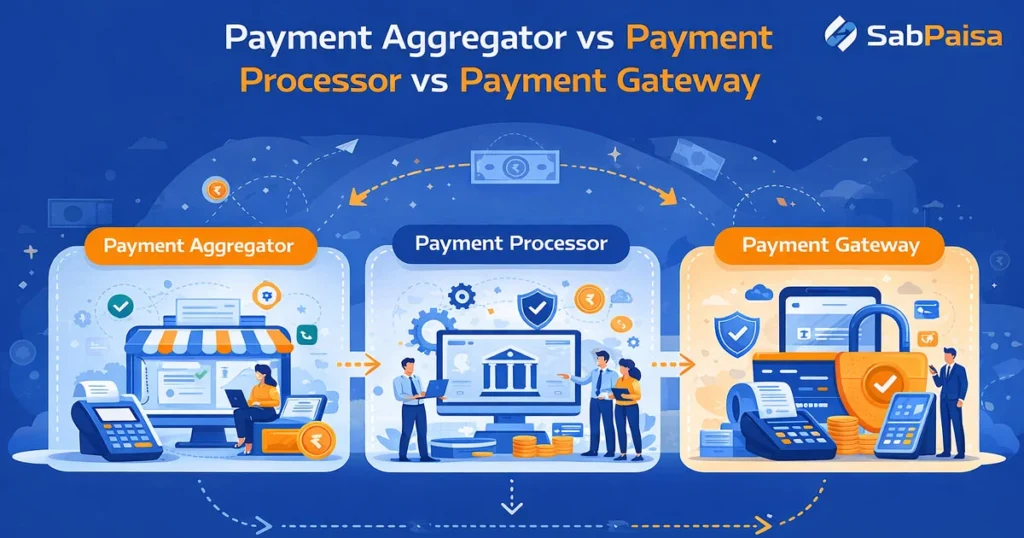

Payment Aggregator vs Payment Processor vs Payment Gateway

Payment gateways and processors are foundational payment solutions in online commerce. A payment gateway is the customer-facing technology that captures and encrypts payment data and transmits it securely to the bank or processor.

- In practice, a gateway (offered by banks or fintech firms) acts as the virtual link between the merchant’s website and acquiring banks, focusing on secure data flow. A payment processor is a back-end entity (often a bank or network) that actually authorises the transaction and moves funds from the customer’s account to the merchant’s account.

- In contrast, a payment aggregator is a third-party service that combines multiple payment methods into one unified platform. Aggregators manage a pooled merchant account, so businesses do not need separate agreements with each gateway or bank.

- In India, aggregators also handle compliance: for example, RBI requires non-bank aggregators to be authorised under the Payment and Settlement Systems Act, whereas pure gateways (which don’t touch funds) don’t need this licence.

In summary, Payment Gateway service providers focus on the technology of data transmission, payment processors handle fund movement and settlement, and payment aggregators (like SabPaisa) bundle payment options and compliance into a one-stop payment solution.Major Indian payment gateway providers illustrate that these gateways offer encrypted checkout flows, while aggregators offer unified APIs and dashboards. When choosing, businesses weigh control versus convenience. Large enterprises often prefer direct gateway+processor setups, while small businesses benefit from the simplicity of an aggregator.

Payment Aggregator vs Payment Gateway: Understanding the Difference

| Difference | Payment Gateway | Payment Aggregator |

| Permission to Operate | Bank payment gateways operate within the guidelines issued by the RBI regarding banks’ outsourcing of financial services. RBI has separate guidelines for technology providers that non-bank payment gateways must follow. | The RBI authorises non-bank payment aggregators under the Payment and Settlement Systems Act, 2007.Entities with a payment aggregator licence granted by the RBI are authorised to provide payment aggregation services to merchants. |

| Payment Options | Payment gateways provide limited payment options. | Payment aggregators provide multiple payment options. |

| Ownership | Banks and other companies generally own payment gateways. There are no capitalisation requirements for payment gateways. | Payment aggregators are generally FinTech companies and financial service companies. Payment aggregators must have a net worth of more than ₹25 crore. |

| Merchant Onboarding | RBI has no specific guidelines for payment gateways concerning merchant onboarding. | For merchant onboarding, payment aggregators must ensure that customer data is not saved in the merchant systems, that PCI-DSS and PA-DSS compliances are met, and that there is a board-approved policy for merchant onboarding in place. |

| Transaction Success | Acquiring banks have multiple payment gateways that merchants can use to route transactions and maintain a high success ratio. | Payment aggregators connect to many acquiring banks, which in turn connect to various payment gateways. This increases the likelihood of transaction success. |

Key Features of a Reliable Payment Gateway Aggregator

Payment aggregators in India have several distinct features that make them a vital component of worldwide digital transactions:

- Payment aggregators provide a secure payment channel and a variety of fund transfer methods.

- They are easy to comprehend and apply, both for customers and business entities.

- Business owners must provide address verification, a PAN card number, and a bank transaction statement, among other documentation, during the onboarding process. The requirements may change depending on the payment aggregator.

- Payment aggregators’ digital footprints assist in preventing fraud and detecting cyber risks.

- Payment aggregators also offer customers discounts and EMIs.

Security Measures Used by Payment Aggregators

Security is paramount for any online payment gateway in India, especially those branded as one-stop solutions. Any legitimate aggregator and gateway uses strong encryption (SSL/TLS) and meets the standards of PCI-DSS.

According to the RBI, every Indian aggregator must adhere to the principles of PCI-DSS and tokenization, i.e., merchants do not keep raw card data. To illustrate, contemporary platforms have adopted tokenization as a means of substituting card numbers with secure tokens and multi-factor authentication to secure user accounts.

The most secure payment gateway websites boast their security certifications (PCI-DSS, ISO 27001, etc.) and do dynamic routing to back-end banks. These include role-based access controls, regular penetration testing, and real-time monitoring of fraud.

Practically, an Indian payment gateway service provider acting in compliance will have automated checks and security policies approved by the board. Aggregators “must store all payment data within India” and use “strong encryption, tokenisation, and role-based access controls” to prevent breaches.

This means customer data cannot be intercepted or misused. Many aggregators also integrate AI-driven fraud tools: for instance, anomaly detection, geofencing of transactions, and 3D Secure checks are common.

Simply, modern payment aggregators provide a single point of payment aggregation that consolidates security, integrating TLS/SSL channels with PCI compliance, token vaults and ongoing audit. All these measures safeguard both merchants and their customers, making sure that customers still feel secure and confident about online payments.

Types of Payment Aggregators in India

In India, payment aggregators are classified into two types: bank payment aggregators and third-party payment aggregators. Let’s look at each type in depth.

1. Bank Payment Aggregator

Bank payment aggregators were the first payment aggregators to enter the Indian market. They have a more conventional design, which complicates the integration procedure. They are also expensive to set up, making it difficult for new and small firms to use their services. As a result, they are often employed by giant corporations.

2. Third-party Payment Aggregators

Third-party payment aggregators entered the market after bank payment aggregators, and they have grown in popularity over time. This is because third-party payment aggregators are more adaptable and offer innovative, user-friendly, and business-oriented payment solutions, making them a popular choice among merchants and business owners.

3. Industry Use Cases

Payment aggregators serve many industries by providing tailored payment solutions. For example, eCommerce payment gateways are critical for online retailers.

- Merchants using WooCommerce or Shopify can integrate a WooCommerce payment gateway plugin from providers like SabPaisa to accept credit/debit cards, UPI, netbanking, and wallets in one go. This simplifies the process of checkout and compliance (no individual bank accounts required).

- In the same manner, creators of content and small businesses that operate on WordPress also integrate a WordPress payment gateway through WordPress payment gateway plugins to enable checkout facilities.

- With the help of a reliable WordPress gateway plug-in, a blogger or freelancer can immediately begin receiving UPI and card payments without any coding.

- Third-party aggregators are also supported by site builders such as Wix. For instance, Cashfree offers a payment gateway for Wix: its Wix plugin enables merchants to accept 180+ payment modes (cards, UPI apps, wallets, BNPL, etc.) on their no-code websites.

- Users simply connect their Cashfree account to Wix and immediately get a full suite of payment methods.

In all these cases, aggregators act as one-stop payment solutions: they provide an all-in-one integration (plugin or API), handle regulatory compliance, and support multiple payment instruments out of the box. This flexibility is used across industries from retail (WooCommerce shops) to services (WordPress professional sites) to events and booking platforms.

By choosing the right aggregator or gateway, businesses on any platform (Wix, WordPress, or custom) gain reliable payment flows with minimal setup.

SabPaisa’s All‑in‑One Payment Platform

SabPaisa is an RBI-compliant, PCI DSS and ISO-certified payment aggregator in India, providing a unified platform for online and offline collections, Payouts, B2B transactions, recurring eNACH, and payment links.

SabPaisa helps education, retail, and MSME companies grow by providing them with real-time reports, robust APIs, a test sandbox, a single, intuitive dashboard, and secure, seamless payment flows that are fully compliant.

With SabPaisa, your e-commerce business gains a robust, secure, and flexible payment solution that enhances both merchant operations and customer satisfaction. SabPaisa stands out with its key differentiators:

- RBI-authorised: It meets the regulatory guidelines and provides a secure environment.

- Hybrid Payment Model: This allows businesses to pay both online and offline.

- Unified Integration: They process payments from a variety of incoming channels with one simple integration for the merchant.

- Frictionless Onboarding: Quick and simple onboarding, getting businesses up and running in no time.

- Secured: SabPaisa is PCI DSS and ISO certified, providing a secure network for both merchants and customers.

In practice, this means a merchant can use SabPaisa’s all-in-one solution to accept a broad mix of payments (credit/debit cards, UPI, wallets, netbanking and even recurring invoices) with a single integration.

Future Trends in Payment Aggregation

The payment aggregation landscape in India is evolving rapidly. Payment aggregators in India are expanding beyond just checkout services. A key trend is the rise of payout APIs and instant settlements.

Modern aggregators are adding tools that let businesses automate disbursements (vendor bills, salaries, refunds) in real time. For example, a Payout API enables a company to trigger bulk payouts programmatically 24/7.

These APIs ensure an instant payout to employees and suppliers by supporting NEFT, RTGS and UPI. By automating payout, businesses can now pay all of their suppliers right out of their system and compensate gig workers instantly without leaving their system. Another focus area is instant refunds and cashbacks, since real-time refunds establish customer trust and loyalty.

In the future, the best payment aggregators in India will position themselves as payment-one-stop options. As an example, Cashfree is a one-stop payments solutions suite that is said to handle recurring billing, reconciliations, and instant bulk payouts on a single platform.

AI will also be used by aggregators to do smarter routing and fraud detection, and will think about blockchain to make remittances across borders quicker. The integration of payer/payee services (within one dashboard) will be a norm. To conclude, the trend in future will focus on programmable and real time money flows.Major aggregators will provide simple payout APIs to transfer funds instantly, add value-added services (such as embedded lending), and keep compliance simple. The major gateways and aggregators in India have the potential to offer much more powerful all-in-one payment infrastructure to businesses, which is consistent with global fintech developments.

Conclusion

Payment aggregators are crucial components of the digital payment ecosystem. They operate as a mediator between clients and merchants, allowing for simple fund transfers. While payment aggregators provide convenient access, transaction flexibility, and secure payment methods, they can also be strict with transaction limitations and account holds. The key is to choose a payment aggregator that meets your business’s requirements.

FAQ’s

1. Can a business use both a payment gateway and a payment aggregator in India?

Yes, both solutions can be implemented for the same-day go-live of a payment aggregator with a custom-built solution (payment gateway) for long-term gains.

2. How do Payment Aggregators and Payment Gateways assist small businesses?

Payment Aggregators can be a cost-effective solution for microtransactions. Payment Gateways can quickly access small businesses when they work with Payment Aggregators. The Payment Aggregator approach provides a platform for online transaction processing with minimal or no start-up costs.

3. What are the compliance requirements for payment aggregators with respect to grievance redressal and management?

Payment aggregators must implement a formal and fully stated consumer grievance redressal and dispute management procedure, according to RBI guidelines.

4. How safe are payment aggregators?

Payment aggregators are highly secure and use digital and data security infrastructure to prevent fraudulent activity.

5. What can a payment aggregator do if fraudulent activity is suspected on a website?

In the event of fraudulent activity or even suspicion of fraud, payment aggregators can either suspend or permanently remove a merchant account, depending on the scenario.